Fill Your Connecticut Probate Form

When a loved one passes away, navigating the complexities of their estate can be daunting. The Connecticut Probate form plays a crucial role in this process, serving as a guide for family members or friends who are tasked with settling the decedent's affairs. This form outlines the necessary steps for filing an Estate Tax Return, which must be completed within six months of the death. It also emphasizes the importance of timely payment of probate charges, which are based on the estate's value. Understanding the responsibilities of the fiduciary—whether an executor named in a will or an administrator appointed by the court—is essential. This individual must ensure that all debts, funeral expenses, and taxes are paid before distributing the remaining assets. The form also highlights the significance of filing the will and any codicils within 30 days of the testator's death. For those dealing with smaller estates, a simplified procedure may be available, allowing for a more straightforward settlement process. Overall, the Connecticut Probate form serves as a vital tool, guiding fiduciaries through the often challenging landscape of probate court procedures.

Documents used along the form

When dealing with the Connecticut Probate process, several key forms and documents often accompany the main probate form. Each of these documents serves a specific purpose in ensuring that the estate is handled according to legal requirements and the wishes of the decedent. Below are five important documents commonly used in conjunction with the Connecticut Probate form.

- Last Will and Testament: This document outlines the wishes of the deceased regarding the distribution of their assets. It names beneficiaries and may designate an executor to manage the estate.

- Codicil: A codicil is an amendment to an existing will. It allows the testator to make changes, additions, or deletions without creating an entirely new will.

- Real Estate Purchase Agreement: This crucial document outlines the terms and conditions for real estate transactions in Texas, ensuring that buyers and sellers understand their rights and obligations. For more information, refer to Texas Documents.

- Application for Appointment of Administrator: If a person dies without a will, this application is filed to appoint someone (usually a close relative) to manage the estate. The administrator will have similar responsibilities to an executor.

- Estate Tax Return: This form must be filed within six months of the decedent's death. It reports the value of the estate and calculates any taxes owed, ensuring compliance with state tax laws.

- Inventory of Estate Assets: This document lists all assets owned by the decedent at the time of death. It provides a clear picture of the estate's value and is essential for both tax calculations and the distribution of assets.

Understanding these forms and their purposes can help streamline the probate process, making it less overwhelming for those tasked with managing a loved one’s estate. Engaging with these documents early on can lead to a smoother administration of the estate and help fulfill the wishes of the deceased in accordance with the law.

Preview - Connecticut Probate Form

Common Questions

What is the purpose of the Connecticut Probate form?

The Connecticut Probate form serves to facilitate the legal process of settling a decedent's estate. When a person passes away, the probate court oversees the distribution of their property according to their wishes, if a will exists, or according to state laws if no will is present. This form helps in filing necessary documents and ensures that debts, funeral expenses, and taxes are paid before any assets are distributed to beneficiaries.

Who is responsible for filing the Probate form?

The responsibility for filing the Probate form typically falls to the executor named in the decedent's will. If there is no will, a close relative, such as a spouse or adult child, may file an application for the appointment of an administrator. This individual will manage the estate's affairs, similar to an executor, ensuring that all legal requirements are met in accordance with state laws.

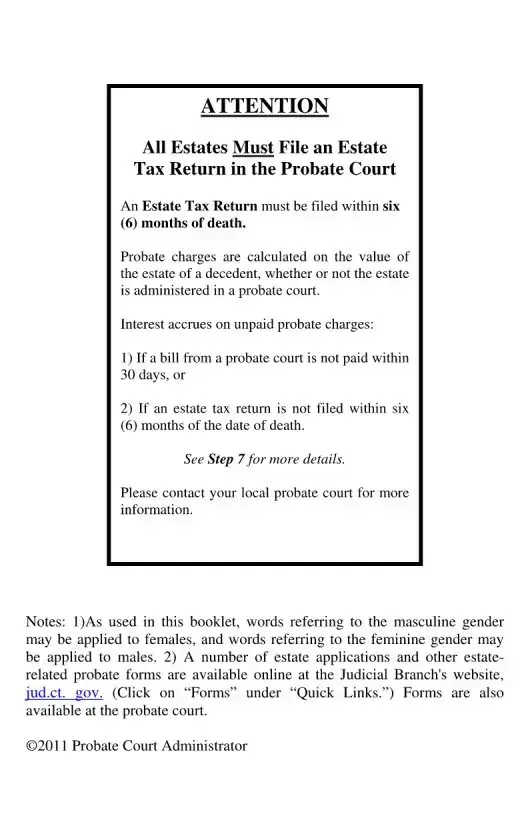

What are the consequences of not filing the Probate form on time?

Failing to file the Probate form within the required timeframe can lead to penalties. Specifically, if a will is not submitted to the probate court within 30 days of the testator's death, there may be criminal repercussions. Additionally, if an estate tax return is not filed within six months, interest will accrue on unpaid probate charges, which can complicate the estate settlement process.

Can small estates use a simplified procedure for probate?

Yes, there is a simplified procedure available for settling small estates. If the total value of the estate does not exceed $40,000 and the decedent owned no real estate other than survivorship property, this process may be utilized. This allows for a more streamlined settlement without the need for appointing an administrator or admitting a will for probate, making it easier for families to manage smaller estates.

When should a fiduciary seek professional assistance during the probate process?

A fiduciary should consider seeking professional assistance when managing an estate that involves substantial or unusual assets or when the estate is large enough to require a Federal Estate Tax Return. Engaging a professional can help navigate complex statutes and tax laws, ensuring compliance and efficiency in the administration of the estate.

Common PDF Forms

Connecticut Coaching Certification - The form emphasizes the importance of safety training in coaching roles across Connecticut.

The simple Motor Vehicle Bill of Sale document ensures that the buyer and seller have a clear record of the transaction, which can be vital for future reference or disputes. It outlines the necessary details involved in the sale, safeguarding the interests of both parties.

Connecticut Withholding Employer Login - Gross wages listed on the original return need to be identified accurately.

Guide to Filling Out Connecticut Probate

Filling out the Connecticut Probate form is an essential step in managing a decedent's estate. Completing this form accurately ensures that the probate court can process the estate efficiently. Here’s how to fill it out:

- Gather Necessary Information: Collect details about the decedent, including full name, date of death, and last known address.

- Identify the Executor or Administrator: Determine who will be responsible for managing the estate. This person is usually named in the will or appointed by the court if there is no will.

- Complete the Form: Fill in the required fields on the form. This typically includes personal information about the decedent and the executor or administrator.

- List Estate Assets: Provide a detailed account of the decedent's assets, including bank accounts, real estate, and personal property. Include estimated values where applicable.

- Detail Debts and Liabilities: List any debts the decedent owed at the time of death. This may include loans, credit card debts, and outstanding bills.

- Review the Form: Double-check all entries for accuracy. Ensure that all required fields are completed and that the information is clear.

- Sign and Date: The executor or administrator must sign and date the form to certify that the information provided is true and accurate.

- Submit the Form: File the completed form with the appropriate probate court within the required timeframe, typically within 30 days of the decedent's death.

Once the form is submitted, the probate court will review it. The next steps will involve further proceedings, which may include appointing the executor or administrator and addressing any outstanding debts or taxes before distributing the estate's assets.

Dos and Don'ts

When filling out the Connecticut Probate form, consider the following dos and don'ts:

- Do: Ensure that you file the Estate Tax Return within six months of the decedent's death to avoid penalties.

- Do: Deliver the will to the probate court within 30 days if you are the executor or have knowledge of the will.

- Do: Seek professional advice if the estate involves complex assets or requires a Federal Estate Tax Return.

- Do: Review all documents for accuracy before submission to prevent delays in the probate process.

- Don't: Ignore the requirement to pay probate charges within 30 days to avoid accruing interest.

- Don't: Forget to include any codicils along with the will when submitting to the probate court.

- Don't: Assume that you can bypass the probate process if the estate is small; verify eligibility for simplified procedures.

- Don't: Delay in filing necessary documents, as this can complicate the settlement of the estate.